The Role of Blockchain for the European Bond Market

This paper provides an in-depth analysis of current inefficiencies in the entire bond issuance value chain in Europe and how blockchain technology could be used to address these issues at stake on top of the existing conventional solutions. In particular, we aim to assess the overall impact from the perspectives of both practical implementation and market participants and thereby employ an approach of combining qualitative analysis with market observations and expert surveys. — Authors: Wanli Chen, Qianxia Wang

Download the article as PDF-File.

Issuing a bond: timeline and key participants

For a stand-alone bond in Euro markets, a typical fund-raising timeframe may range from three weeks to more commonly six weeks (Adams, 2016). The process consists of two phases, pre-issuance and post-trade. The pre-issuance includes the preparation of issuance, choosing the modalities of the price discovery mechanism (syndication, auctioning, or private placement) and striving agreements between the issuer and investor on the economic terms of the securities. Taking place after the pre-issuance, the post-trade process includes the actual issuance of the debt security in central securities depositories (CSDs) and its delivery to investors via global or local custodians, agent banks and other intermediaries each representing different issuers or investors through multiple distribution channels. As an integral part of the financial industry value chain, post-trade services involve crediting the proceeds of the issuance of financial instruments to the issuer’s account upon related post-trade services have come into play, and executing trading counterparties’ agreement to buy or sell, resulting in a change of ownership.

In order to generate a clear overview of the market participants and their relevant roles, we have divided the descriptions into two parts: table 1 provides brief descriptions of key participants’ roles and their missions for the pre-issuance stage, and table 2 shows the same information for the post-trade stage.

The post-trade process takes place after the pre-issuance phase. It includes the actual issuance of the debt security in central securities depositories (CSDs) and its delivery to investors via global or local custodians, agent banks, and other intermediaries, each representing different issuers or investors through multiple distribution channels.

Existing inefficiencies in the pre-issuance process

The pre-issuance includes the preparation of issuance, choosing the modalities of the price discovery mechanism (syndication, auctioning, or private placement) and striving agreements between the issuer and investor on the economic terms of the securities.

From the standpoints of dealer banks. A majority of respondents to our conducted survey from dealer bank origination indicated that the manual-intensive work is one of the main causes for inefficiency: “there is no or quite no digitalization in pitching phase and contract phase”, “manual effort in preparing pitching docs and contract, preparing signing”, and specifically, an experienced Know-Your-Costumer (KYC) officer pointed out that the pre-issuance phase contains “manual effort in documentation preparation and verification, plus it is lack of harmonization and time-consuming.”

Particularly in the underwriting process, a lot of back and forth discussion that occurs among the lead managers, issuers, syndicates, and investors as the latter seek to understand the deal structure, credit quality, and industry dynamics. The communication usually happens via email and Bloomberg chat, which means there is no one data room to store documents and that it is hard to keep track of information flow in the future. As a specialist in the green bond origination space pointing out:

“Relevant documents (prospectus, term sheet, green bond framework, and green bond second party opinion) are sent via email. This makes it difficult to keep track of documents and results in extensive email traffic.”

Furthermore, the lack of standardized information storage practice also leads to reconciliation inefficiency. Particularly in book-running process, salesperson negotiating in private conversation with prospective investors, investors submitting bids via fax/email/telephone, trading desk accumulating bids in a spreadsheet, and information sharing with investors via separate digital channels are resulting in multiple versions of the truth. Since each participant maintains its own version of record, a time-consuming reconciliation process between participating systems will need to be continuously executed to keep everyone in the same status quo (Capgemini consulting, 2016).

From the standpoints of investors. Data referencing is another major pain point. In current practice, multiple identifier systems are used, and the process of obtaining security identifiers slows down the speed for trading in the secondary market to some extent. For instance, while a substantial amount of securities worldwide is assigned with an ISIN number, the most commonly used identifier for stocks and bonds in the US and Canada is CUSIP, and in the UK SEDOL is more recognizable.

Another inefficiency in the information flow is reflected by the fact that the distribution of deal terms to investors requires human intervention, and the process is not always optimal. For one thing, bank syndicates determine which salespeople to send deal terms to, and those salespeople determine which investors to send to, resulting in that some investors may not see deals that they might be interested in. For another, salespeople typically distribute deal terms to rather static distribution lists, which can be a laborious process for salespeople who are progressively focused on providing value or insights to the buy-side in a resource-constrained environment (IHS Markit, 2019). An experienced individual from a dealer bank syndicate team further stresses this issue at stake:

“…the amount of information needed varies also. Frequent and well-rated issuers are well-known, and investment decisions by investors also depend on the overall market backdrop, whereas bond issues from non-frequent and/or high yield issuers need to provide a lot more information in the run-up to a bond issue. The lower the rating scale, the more deal-specific information is needed.”

From the standpoints of issuers. According to a data specialist, “current practice will contribute to a good relationship between issuers and banks likewise investors and banks as well as direct feedback (including nuances in answers/tones) due to personal contact”. Thus, it is pointed out by a public issuer’s quantitative analyst that the unbalanced flow of knowledge results in the situation that “information about investors is often of poor quality”, along with the yet-to-be-developed “investor identification and classification” system.

Another notifiable inefficiency revealed by a funding officer from the public issuer’s side is described as the following:

“When preparing syndicated issuance, the potential bank contacts are limited. It depends on other factors like how many need to be contacted and how these are selected, but in public institutions, this is more linked to internal policy (need to justify the choice) than any-thing else. Inefficiencies are more linked to this “political” angle, which cannot be avoided in my view.”

From the standpoints of overall EU debt capital market (DCM). On a higher-level view over the European debt capital markets, inefficiencies are also incurred from the fragmentation of existing EU distribution ecosystems. In the current debt distribution practice in the Eurosystem, there is no pan-European issuance platform like in other major currency areas, e.g., US, Japan, or China, where domestic issuance distribution channels exist (EDDI consultations, 2019). Various networks in the EU are based on a hierarchical model and maintain privilege for the initial issuance location, which may compromise the level playing field and hence impact the equal access to the European debt securities by investors. Many market participants only use national structures and solutions, limiting the efficiency with which capital is distributed and transferred across Europe. Moreover, the lack of a standardized EU tax and securities law, different levels of disclosure requirements, and multiplicity of non-interoperable issuance platforms and proprietary procedures with a very low level of automation and digitalization are posing challenges to a harmonized European DCM market (AFME, 2019; ICMA, 2018).

While the well-diversified source of financing with stable and predictable costs represents an excellent opportunity for both issuers and investors, the term “home bias” implies that issuers might face additional barriers to place bonds outside their domestic country. As a result, they would need to bear additional costs if domestic conditions determining the pricing of their bonds were less favorable than those prevailing in international markets (Lau, Ng, & Zhang, 2010). In addition, home bias might make it harder for corporate bond markets to act as diversification of investments if domestic banking stress is accompanied by wider stress in domestic markets (ECB, 2018).

Existing inefficiencies in the post-trade process

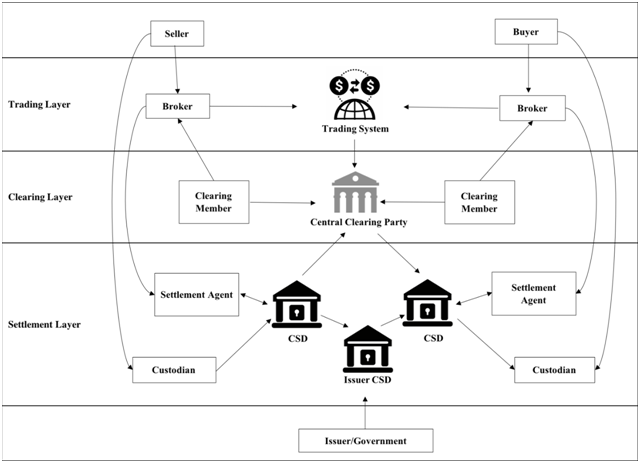

The current post-trade landscape involving multiple financial intermediaries can be generally divided into three layers: trading layer, clearing layer, and settlement layer, as shown in figure 1, where market inefficiencies arise from several perspectives.

First, financial intermediaries keep multiple separated records of the same information, and they have to update their own accounts every time a new transaction occurs, which creates a redundant workflow and additional risks. The lack of interoperability between centralized database systems restricts straight-through processing for a range of non-vertically integrated financial institutions across the three layers. In addition to widening the settlement cycle and increasing the cost of back-office procedures, the need to reconcile information kept in different intermediaries creates certain risks, such as failures in settlement chains, human errors, and limited collateral fluidity (Pinna & Ruttenberg, 2016).

Second, the payment chain throughout the bond’s life-cycle is rather complicated and costly. Consequently, payments will have to go from the issuer to the paying agent to the clearing systems and then possibly to one or more custodians before it eventually arrives at the person entitled to it. Some market participants also choose a trustee to represent the bondholders and protect their interests.

Third, concerning legal workflow, the documentation process of a traditional bond issue is relatively complex and cost-inefficient. The terms of the global certificate clarify that, while the nominee holds legal title, the account holders in the clearing systems hold the beneficial title. The split between legal and beneficial title to the bonds is realized by entering the name of a nominee into the register, evinced by the issue of a global certificate, which characterizes the entire issuance. The documents also make full provision for the issue of definitive certificates, which would be issued to individual investors in certain situations, including if the clearing systems ceased to function. This would involve entering each account holder into the register. The association between the issuer and the registrar, and the issuer and the paying agent, also need to be contracted and documented. For capital markets practitioners, there are standard procedures, but for an issuer that has never issued a bond before and wants to understand and access the market, it can be a time consuming and costly process (Cohen, Smith, Arulchandran & Sehra, 2018).

From a higher-level point of view, the current infrastructures lack full financial integration and the EU-wide risk sharing of a single capital market. Currently, there is no option available in Europe that allows issuers to reach their European investors in a neutral (without home bias) and standardized way. Instead, issuers and investors rely on a network of connections between different national CSDs or on international CSDs and the services, tools, and procedures provided by large custodian and dealer banks. Thereby, the securities issued always reflect a specific home bias, and thus they are not truly “European”. Even though this model functions well for national issuance, it is suboptimal when seen from an all-embracing European perspective.

Conventional solutions under development

Conventional solutions for the pre-issuance process. To foster standardization and harmonization in the pre-issuance process, various initiatives have been exploring solutions to stress the inefficiencies and fragmentation in the current European environment.

IHS Markit, the acquirer of Ipreo, provides a set of services to more than 180 banks worldwide, especially in the pre-issuance context that offers substantial benefit to market participants in terms of standardization and harmonization. For instance, its IssueBook and IssueNet products provide a pre-issuance platform that enables banks to price deals faster, removes risk from the pre-issuance process, and has also implemented many innovations that have benefitted the industry such as unified book building and standard deal terms. IHS Markit’s IssueLauch solutions also contribute to the harmonization by developing a set of mandatory deal terms in consultation with banks and investors and using embedded logic to certify that deal terms reach the correct investors and critical sales team resources are optimized. This has been adopted by the market and is so far used on 95% of Euro-denominated investment-grade deals (IHS Markit, 2019).

Project Mars is a private sector initiative aiming at modernizing the process of corporate bonds issuance and streamlining the information exchange flows in the primary debt market (Bloomberg, 2019). The project will initially focus on the US investment-grade bond market in 2018 (Bloomberg, 2019). The project was initiated by a consortium of three multi-national investment banks and had a similar service offering from its rival platform — Ipreo. However, Ipreo has difficulties entering the US market compared to its success in Europe. According to IFR International Financing Review (2018), major US players are concerned about the ownership of Ipreo and its potential monopolistic market position as a single fixed income service vendor.

European Distribution of Debt Instruments (EDDI) Standardised Toolkit is a technical toolkit brought out by the European Central Bank’s (ECB)’s EDDI initiative that aims at creating a pan-European issuance mechanism to promote a single domestic market for Euro debt instruments distribution and harmonizing the currently fragmented market structure. Specifically, the technical toolkit will be available for issuers (or their issuer agents and/or dealer banks upon authorization) offering them functionalities which support the definition and communication of an upcoming debt issue, the creation of the order book, the collection of orders from investors and the allocation of the debt instrument issuance to these orders (EDDI Consultation, 2019, see figure 2).

Conventional solutions for the post-trade process. In the efforts of promoting an integrated European post-trade landscape, harmonization in infrastructures and regulations have taken place in the past decades.

Target2-Securities (T2S) settlement platform is now the predominant platform and is expected to cover a total of 21 European countries and settle almost 100% of securities transactions in Euro central bank money. T2S affects not only the payment and settlement layers but also the clearing and trading layers. In order to settle transactions via the T2S platform, a market participant needs to hold a security account with one of the participant CSDs and a committed cash account with one of the central banks on-board to the platform. These accounts sit alongside on T2S and are matched when the instructions from the CSD and the central bank come in. T2S then settles the transaction on a delivery-versus-payment (DvP) basis using central bank money, which means the cash and securities change hands simultaneously. As a result, not only investors from the same CSD can realize instant settlement, but also investors account from different CSDs and jurisdictions can also achieve settlement on the same efficiency. Currencies other than Euros can also be used for settlement as long as the concerned central bank adds it to their brackets.

CSD Regulation (CSDR) is the newest major piece of EU infrastructure legislation launched in 2014 to improve the securities settlement process in Europe. It introduces a common authorization, supervision, and regulatory framework for CSDs. Alongside the European Market Infrastructure Regulation (EMIR), Markets in Financial Instruments Directive (MiFID) I / MiFID II, and Markets in Financial Instruments Regulation (MiFIR), the implementation of CSDR complements the regulatory framework for the transaction life-cycle.

Although CSDR has not yet been fully developed and implemented, it has made some notable achievements in addressing market inefficiencies:

- Long settlement time: the CSDR has already had some effects, including adoption in all European markets of the trading day plus two days (T+2) timeline for the settlement of securities transactions. The dematerialization/immobilization of securities is promoted together with the usage of central bank money for settlement of securities transactions.

- Interoperability of current platforms: Optionality of degrees of account segregation at CSD level and the harmonization of finality rules (at three different stages of the settlement process) are also introduced.

- Fragmentations in current structures: CSDR addresses the existing fragmentation in the process of handling settlement fails in the EU by imposing mandatory buy-ins. Detailed rules on the buy-in process are in development.

In the light of blockchain, traditional physical bond certificates or notes can be substituted by digitalized debt instruments that can be directly issued on the distributed ledger.

Blockchain bonds

Beginning with the Bond-I issued by the World Bank, we have witnessed more and more pilot projects initiated in order to test or to experiment with the performance of blockchain technology in combination with the traditional financing process. Blockchain technology has demonstrated its massive potential to enhance the current outlook.

Starting from creation, allocation, transferring to management, the entire life-cycle of blockchain bonds takes place on distributed ledgers. During the bond issuance process, blockchain technology could enable real-time book building, but also direct dealings and communications among issuers, lead managers, syndicate members, and investment banks. Hence, smart contracts can further enhance the execution automation with respect to the terms and conditions encoded in the smart contracts. In addition, both securities and cash can be tokenized in order to streamline and speed up the clearing and settlement process. As a bond issuance is a strictly government-regulated activity, several premises need to be considered.

- Specifying the digital bond token including the type, value, size, ownership, terms and conditions, and actions of the debt instrument

- Ensuring regulators’ access to the transaction blocks for the monitoring and audit purposes

- Providing due diligence mechanism to prevent financial fraud or abuses (e.g. KYC workflow), given the fact that procedures vary depending on the security type and nature of the issuer and its business

- Identifying on-chain currency for the cash tokens (e.g. adoption of fiat-collateralized stablecoin)

A potential blockchain solution design shown in figure 2 is constituted by the following steps:

a) The issuer issues the bond in tokenized form into the asset ledger

b) Approached by the issuer, investment banks initiate a digital term sheet and receive sign-off from the issuer

c) Lead manager and syndicate members have individual single views on the master book regarding bids and orders from the potential investors

d) In order to add investors into the bond blockchain, issuer seeks KYC details of investors which are provided by the gatekeepers/intermediaries

e) Fund managers hold tokens that record investors’ holdings, either cash or debt instrument. Tokens will be used when settlement occurs

f) Transactions take place when the deal comes to the closing stage after signing. During settlement, custodians or banks will act as token keepers and transfer money/debt instrument to the beneficiary accounts based on an instruction

g) Cash is tokenized in the cash ledger to facilitate and complete buying or selling

h) Via on-chain delivery-versus-payment, near real-time settlement, can be achieved in the blockchain network. Instead of physical certificates, debt instruments will be credited to the corresponding investors’ accounts in the digital token form

i) Smart contracts automate the execution of corporate actions, such as dividend and coupon payments, interest, the return of capital, etc.

j) Via the observation nodes, regulators are able to access directly to the detailed transaction data so that they can provide a live audit trail. Thus, they will be able to monitor and investigate the transactions and the blockchain platform activities to ensure they comply with legal and regulatory requirements.

Potential blockchain impact on pre-issuance

In our survey, several syndicates brought up a common opinion that

“Nowadays, pre-issuance is still highly manual dependant regarding preparing pitching docs and contracts, as well as preparing signing. Depending on the risk profile, nature of the business, and frequency of issuance, the amount of information varies for different issuers.”

Observing the capital market, existing conventional solutions such as Ipreo and EDDI have explicitly worked on standardization of information and communication, workflow streamline in book-running and allocation. Nevertheless, a head of e-trading responded in our survey that

“Digitalization or automation could help finding reliable patterns and strategies for given market/investor/issuer situations. Blockchain will play a massive role, most importantly, in the allocation and booking/delivery/payment process. However, the pre-issuance could stay more face to face, at least in situations where issuers try to place certain kind of bonds or unpopular maturities for the first time.”

Eliminating physical documentation. Traditional bond issuance processes involve a significant number of physical documents related to underwriting, subscription and distribution, and documents regarding the constitution of bonds. By opting blockchain technology/distributed ledger technology (DLT), documents can be stored in the hashes on-chain more digitally and verified only by the authorized users on the blockchain. Therefore, a substantial number of related documents in the physical form can be eliminated. Moreover, the digital form of documents can efficiently prohibit issues raised from the physical form, such as delays, inefficiencies, tampering and errors.

Creating a single source of truth. A syndicate mentioned in our survey that “Information is exchanged verbally, which makes the data unreliable and difficult to cross-check.” Currently, each financial institution owns their individual view of the record which leads to data inconsistency.

Instead of using various identifiers as in current practice, blockchain promotes the single source of truth in the network via the creation of a unique referenced data record system with a unique identifier, which can be shared and viewed in the network in a real-time manner. Essentially, overcoming pain points caused by mismanaged data could eliminate internal and external data reconsolidations and keeps everyone updated on the same status quo. With a streamlined workflow, participants could focus on more value-added tasks. Eventually, it results in lower administrative costs, reducing traditional manual workflow and speeding up the process, especially the book-building process and order transmission.

Enabling more transparent and standardized process. With direct dealings and communications among issuer, investment bank, lead manager, and syndicate group, blockchain solutions allow documentation creation, deal structuring, price negotiation, and order transmission to take place in the same network. Firstly, lead managers and syndicate members have individual access to the real-time master book for book-running instead of the current manual accounting book-entry in excel. Documentation creation regarding pre-terms and conditions could be automated via smart contracts. A chief executive officer (CEO) from a private financial institution stated in our survey,

“If we just get the standardization done, it would speed up the process and shorten the time horizon by providing documentation over smart contracts […], which make everything more efficient and transparent.”

Secondly, salespeople gain easier access to investors for communication and marketing purposes while in compliance with regulations. Thirdly, the issuer gets better insight into the deal structure regarding the potential investors and their positions. Technological innovations are more likely to develop in a competitive environment and spur increasing order flow (Learner, 2011). Increasing visibility for pricing and execution driven by blockchain technology can simultaneously provide better price discovery experience and clarity to the investors. Blockchain solutions create a more competitive environment with greater participation and trading volume, which minimize the risk in underwriting, lower transaction costs, and spreads.

Along with all different workflows of all pre-issuance participants, regulators can easily access the transaction details to prevent financial misconduct and crimes. Real-time monitoring by the regulators leads the pre-issuance process to be more secure and compliant.

Facilitating KYC/client on-boarding. A quantitative analyst concluded that “A lot of manual efforts need to be invested to on-board investors due to the poor quality of investors”. Facing these challenges, blockchain provides two alternatives to facilitate the current complex and time-consuming diligence/KYC process. Firstly, participants, especially issuers, can access the KYC data of the investors via an independent third party (ITP) that provides official and consolidated KYC. Secondly, the individual bank of the consortium group can share KYC checks directly with the other members in the mutual accessible ledger. In order to improve the current time-consuming due diligence workflow, a KYC officer from an investment bank stated a possible solution that

“In fact, 70% of the investor bases among all banks are the same. Instead of each bank conducting their own KYC, an assigned third-party can provide a summary of findings/comments to all banks on a centralized distributed ledger. Once the summary is validated, all participants in the network receive notifications instantly, and the regulator can monitor the performance or effectiveness of the third-party service provider.”

Broader access to the capital markets. Contrary to the traditional financing channels, the decentralized finance (DeFi) applications have demonstrated the possibility to provide market participants with better access to the lending pool and significantly reduce the barriers to the financial markets. Adopting blockchain, issuers could enjoy better access to a broader range of target investors and face reducing obstacles for cross-border transactions.

Potential blockchain impact on post-trade

A current lengthy post-trade cycle involves multiple counterparties such as custodians, agent banks, central securities depositories CSDs, and central counterparty clearing houses (CCPs). Crowded with various intermediaries and lack of automation, the current post-trade infrastructure set-up remains highly complex and fragmented. Facing the current challenge, DLT/blockchain technology has the potential to disrupt the current clearing and settlement cycle and reduce significantly transactional and operational costs. Thus, blockchain solutions are most likely to create tremendous effects on setting up a standard for financial transactions, automating the lengthy process without manual intervention, and achieving real-time settlement with the involvement of substantial reducing intermediaries.

Tokenization and real-time settlement (DvP). The ultimate goal for the settlement cycle is to achieve a real-time settlement. In order to apply blockchain technology to achieve this goal, DvP and immutability of blockchain are the two key challenges that need to be considered for the design of the new process set-up (Committee on capital markets regulation, 2019).

In order to achieve DvP, tokenization is under consideration for clearing and settlement in the financial services industry. Settlement coins such as stablecoins have been recently developed and introduced in permissioned blockchains. The stablecoins are pegged to fiat currencies, and settlement would occur in fiat currencies. With both stablecoins and securities represented on the same blockchain system, transactions written into a block would include the security transferred from issuer to investor, and the stablecoin transferred from investor to the issuer. In practice, the majority of issuers is rather global than EU or Euro market issuers (AFME, 2019). Adopting the tokenization of central bank currencies could eventually advance multi-currency settlement services and facilitate cross-border transactions.

Blockchain technology could also work on alternative solutions that allow automating voiding or reversing transactions under certain circumstances. For instance, different markets or security types require some specific operating schedules due to some local specifications (ECB, 2019). The immutability of blockchain records can be eased in the permissioned blockchain structure by embedding with trusted permission nodes that have rights to void or reverse the transactions or writing conditions into smart contracts (Committee on capital markets regulation, 2019).

Compared to conventional settlement procedures, centralized T2S, or TIPs, blockchain technology can effectively mitigate the issue of “single point of failure” with its decentralized feature and guarantee a 24/7 electronic audit trail for the transaction activities. A complex blockchain structure enables possible real-time settlement with improved speed, drive the post-trade landscape more resilient and automated. It can also significantly reduce operational costs and optimize liquidity management. Eventually, implementing blockchain technology in the post-trade process frees up potentially billions of capitals held as collateral.

Automation and better asset servicing. Incorporating blockchain technology in post-trade results in declining reliance on manual processes and prevents manual frictions and errors. Smart contracts would enforce the auto-execution of pre-defined terms and conditions, as well as confidentiality agreements before the transactions.

Corporate actions (i.e., coupon payments, interest, dividend payments, the return of capital, splits or mergers) remain complicated in Europe due to the difference of tax regimes and securities laws. Such particularity of the European post-trade landscape has built barriers for some financial institutions to adopt the conventional solution T2S. Based on the ownership of the asset or fiat tokens in the blockchain, corporate events could be encoded into smart contracts and auto-executed while keeping all members of asset and cash account updated. Especially in the case of Finledger, Germany’s first blockchain-based platform for processing promissory note loans, executions of business confirmation, document creation, certificate changes, assignments as well as redemptions can be digitally realized in the ledger. Simplifying the complexity by automation, blockchain technology could also reduce current operational, systemic risks, and administrative barriers linked to the manual and multi-step process.

With multiple cryptographic signature protection, tokenization provides a more secure and digital asset safe-keeping set-up. To promote and implement comprehensive market standards for the token markets, International Token Standardization Association (ITSA) currently works on providing a unique international token identification number (ITIN), detail token classification, and database for analysis purposes. Attaching a unique identifier for both security and fiat tokens used in transactions enhances operational efficiency, infrastructure simplification and reduces administrative costs.

Substantially reducing intermediaries. With the automation and near real-time settlement, the functions of intermediaries such as central counterparty clearing CCP and a series of back-office agents (i.e., paying agent, issuing agent, bill & deliver agent) would be faded. Lack of transparency of the current process is caused by the fact that different intermediaries are working on different systems, and a market standardized workflow is challenging to be implemented. The new technology could help to eliminate counterparty risk, reducing the administrative cost of holding assets, and driving the process more transparent with more streamlined layers.

Changing roles of market participants

Through the entire issuance life-cycle, blockchain adoption and overall IT development could also have an evolutionary impact on each participant’s role and daily work. Based on the survey of the key market participants and the observation from current market initiatives, we have assessed and evaluated the potential impact on each player in the debt capital market.

Issuers. Blockchain/DLT solutions could help to create a B2B platform that brings investors and issuers together without the involvement of intermediaries. Meanwhile, issuers could gain complete transparency of the entire bond issuance life-cycle taken place in the ledger to better monitor the deal preparation.

With an elaborate KYC set-up in the ledger, issuers make much fewer efforts for the KYC in order to on-board the investors in the future. A higher degree of transparency and rigorous compliance check leads to reducing administrative costs for raising capital and better access to the investors for the securities servicing and transmissions.

Lead manager and syndicate members. Blockchain solutions bring standardization and simplification to the entire process. With a unified view of a master book, manual workflows for periodic basis data reconciliation would be eliminated, and the process would be more streamlined. Thus, data consistency could create a single source of truth and leads to reducing operating costs for the process. Several syndicates mentioned in our survey that “data mining and assessment would become more critical to advise the issuers for the deal structure.” Also, a trader mentioned that “technical innovation especially the implementation of smart analytics will boost the importance of the processes and teams working around trade/client/competitor analysis” Besides, salespeople could gain better access to investors for marketing and communication while in compliance with regulations. Despite the importance of data management, our survey participants also mentioned that “human-based phases (i.e., pitching phase and contract phase) and more senior, as well as relationship-focused positions, would not be impacted much.”

Legal advisors. Similar to dealers, the law advisory service will not be simply replaced by technology, but instead, switch to the focus of standardizing contract terms in order to automate the documentation process. The real value-added work lies in the client’s advice and negotiation of additional terms, conditions, and covenants that impact the performance and enforcement of the financial instruments. Lawyers should not be expected to code legal logic into computers to automate contract creation, but instead, they should contribute to streamlining the process by standardizing and marking existing legal documents so that the terms can be read and understood by computers.

Focused on the utilization of tokens, legal advisors should consider different definitions and requirements for cross-border transactions in the post-trade stage. A case-by-case analysis should be included for each transaction as a harmonized regulatory landscape requires more effort and time.

Custodians or sub-custodians. From a medium-term perspective, market participants do not see complete disintermediation as an option linked to the integration of blockchain technology. Their roles and functions may change and narrow to token custody linked to real-time settlement. Instead of safe-keeping securities, custodians safe-keep and transfer corresponding dematerialized debt securities (i.e., debt tokens) and payment tokens (i.e., fiat-tokens, stablecoins). Meanwhile, custodians would also need to ensure the proper functionality of automated securities servicing in the future.

Intermediaries. The functions of a substantial number of intermediaries such as settlement agents and clearing members would be gradually faded and no longer needed in the bond issuance process due to the automation achieved by blockchain solutions.

Investors. In the pre-issuance phase, investors could potentially have better access (i.e., standardized common platform/interface for data sharing) to all relevant information of the issuers and the corresponding debt securities. Higher transparency in the process can simultaneously provide better price discovery experience and deal clarity to the investors. In the post-trade stage, they would benefit the process efficiency driven by automation, especially in the execution of corporate events.

Regulators. Regulators could access a 24/7 live digital audit trail. Regulators would not only monitor dedicatedly the publicly accessible transaction records but also workflows in the blockchain. They could further enhance their abilities to investigate and prevent market manipulations, unfair pricing, financial fraud, and abuses in a real-time manner.

Challenges — limits of adoption

Regardless the benefits and opportunities brought by the technology, maintaining security and stability of the financial system should also be considered along with the emergence of blockchain technology. On the one hand, there are some limits of adoption due to different technological capacities and interests of market participants. On the other hand, the development and adoption of blockchain remain questionable regarding how they can integrate into the regulatory landscape and what is the role of law in the ledgers.

Technology challenges. Particularly in the financial services sector, most stakeholders or consortium groups would opt for either private or public permissioned blockchain to improve their workflow and to facilitate information and transaction flows. Despite the view on how blockchains will bring tremendous value to the processes, most of the permissioned blockchains require a significantly high level of technical skills and core infrastructure set-up in order to enable its effective functions (Rodriguez, 2019). In other words, it is directly linked to the IT talents within the organization and the investment size in technology at the early stage.

Even though there are already some relevant protocols and tools under development to overcome the technical implementation barriers, individual participants still resist since opting blockchain technology/DLT entails a significant investment in IT, but the benefits remain difficult to be estimated and quantified precisely. Especially in the post-trade stage, A CEO of financial institution mentioned in our survey that “at the moment, I do not know a blockchain protocol which is stable enough to handle all that volume.”

Most importantly, participants need to restructure their technology platforms and set up a robust plan to buffer against technological risks (i.e., systemic shocks) to incorporate the blockchain/DLT technology and achieve an effective functionality of the ledger.

Technical innovation could potentially result in execution risk and oligopoly market structures.

Conflicts of interest. Blockchain can potentially redirect economic interactions away from traditional channels (PreSale Ventures, 2018). Compared to fintech companies, financial institutions might have different interests as they belong to the traditional channels and stand at a strong priority position for decades. With the appearance of DeFi applications that provides market participants with the possibility of equal access to the financial markets, a current barrier (“home bias”) faced by issuers can be gradually reduced as well. Thus, it evidences that new technology can threat the traditional investment banking area. Especially for the traditional financial institutions, maintaining the status quo would better protect their current advantages of the business. That is the reason why some of them resist adopting blockchain technology for their daily business. Regarding the responses to EDDI consultation from AFME, many members consider current manual workflows in the pre-issuance system function smoothly, and such fragmentation does not cause any adverse effect on the market. If there is a lack of cooperation and motivation of core market participants, the effects of blockchain technology seem to be meaningless.

Further, increasing transparency represents either benefits or costs for different market participants based on an analysis of transparency in European bond markets conducted by Learner (2011). On the one hand, greater transparency enables better investor protection and improved market efficiencies. Investors can benefit from a better price discovery with more robust information and improved access to the market. Ultimately, it stimulates competition among market makers and dealers and results in lower bid-ask spreads and transaction costs. Additionally, regulators could enhance their abilities to investigate and prevent market manipulations, unfair pricing, market fraud, and abuses. On the other hand, effects can be adverse for the brokers/dealers due to the strengthened competition in the market. Better price discovery of investors leads to higher costs for dealers to hedge their positions. Thus, issuers, especially in the public sector, may raise concerns regarding KYC fulfillment/client on-boarding responsibility since investors have direct access to approach to them (ICMA, 2019). In reality, for those who act as government bond auctions backstops, increasing transparency may hamper the liquidity provisions at the auctions (Learner, 2011).

Additionally, blockchain stands for a source of growth, along with risks, conflicts, and instability of the market (PreSale Ventures, 2018). In our survey, a syndicate from a European primary dealer bank mentioned,

“Technical innovation would definitely drive the data mining and assessment more important to advise issuers. Nevertheless, it will also increase volatility, shrink the importance of intermediaries, or will shift the business to a few major global operating banks/global asset managers.”

In order to maintain the stability of the market, other market participants who responded to EDDI consultation have argued that “any new technological set-up, infrastructure or platform should be based on complementing the current market infrastructures instead of creating disruptive changes.” (AFME, 2019)

Regulatory and legal issues. Blockchain’s integration into the regulatory landscape remains specifically as a challenging and debatable topic for the issuance of securities (Capgemini consulting, 2016). In nature, regulations play a critical role in addressing risks (i.e. cybersecurity and data privacy protection) and ethically allowing innovation. Since the issuance of debt securities is a government-regulated process, market participants should take careful consideration and understand the evolution of regulatory guidance before adopting blockchain technology.

In fact, legal, tax regimes and regulatory requirements vary greatly under different jurisdictions even though the EU is a political and economic union. Thereby, it results in the fact that nodes are distributed across different legislations. On the one hand, countries under different legislations have different regulations of the capital market. For instance, in order to achieve a pan-European project (e.g., EDDI), concerns regarding cross-jurisdictional issuance have been voiced due to differences in prospectus regulations, tax and fiscal systems, fund regulations, notary requirements, and national government auction mechanisms. With such an undoubtedly complex legal environment, the choice of governing law for the contractual relationship among participants in the blockchain network remains hard to be decided.

One of the major concerns raised by the ECB regarding blockchain/DLT usage is about how network operators will comply with national provisions on professional confidentiality and secrecy. In practice, there are different data and information privacy protection laws applied to information storage and transmission around the globe — one of the key usages of blockchain. For example, information privacy is much more restricted under the General Data Protection Regulation (GDPR) in Europe than under the US privacy model, since data privacy is not highly regulated and legislated in the US. Regarding the confidentiality issue, jurisdictional variations can consequently result in participants’ reluctance to adopt the technology while taking the risk.

Another issue is the legal enforceability of smart contracts (Mathias, 2018), as legal justification of smart contracts remains unclear (Valenta, Sandner, 2017). So far, smart contracts are not necessarily contracts by legal definition. Although there have been efforts driving the smart contracts accurately reflect the written legal contract (Peters & Panayi, 2015), a common question such as “is code prevailing on the law?” is still raised frequently.

Despite the challenges, Europe has been actively involved in promoting the integration of blockchain technology and building a necessary regulatory infrastructure to simplify and facilitate the issuance of security tokens. Nowadays, security tokens are regulated as securities under MiFID II. Security tokens such as debt tokens could be potentially treated as “transferable and negotiable securities” (Steis, 2019). Since the beginning of 2019, the German financial regulatory authority BaFin has already approved two STOs that work like bonds for two German fintechs to raise funding. Other EU nations have also started to actively participate in the regulatory harmonization of blockchain integration based on various indications, marketing, addressing investors and sales. Regardless of the current efforts, the approval of security tokens remains case-by-case in the Euro area. However, standardized strategic guidance and frameworks to regulate and monitor STO/securities issuance on DLT are still under active discussion.

Summary

With the application of blockchain technology, the bond issuance process could be driven towards an innovative path in both the public and private sector, achieved by enabling smart contract-led automation, reduction of intermediaries, automated asset-servicing through a distributed ledger and 24/7 electronic audit trail along with the various phases. Given the potential streamlined process and workflows, blockchain technology could be a signi-ficant endeavor that digitalizes the bond issuance process, integrates European debt capital markets, and shifts major market participants’ role in the value chain.

Regardless of the opportunities created by adopting blockchain technology, there are some challenges in the practical implications. Firstly, regulations, legalizations, tax regimes, and data protection laws vary under different jurisdictions in the European market. In the blockchain set-up, many other complexities need to be tackled to establish more sophisticated solutions for multi-regional and multi-time zone accessibility and governance structure while in compliance with different regulations. Secondly, technology adoption needs to win massive support if it aims to change the market infrastructure or behavior. In order to maintain the stability of the debt capital market, market participants have urged that technology should focus on creating efficiencies and value for the current set-ups and infrastructure instead of completely replacing them. Hence, blockchain adoption should not cause a complete disintermediation effect as human interactions in the advisory functions are still necessary, especially for the deal negotiation in the pre-issuance process. Most importantly, blockchain should not be considered as a single solution to improve issuance efficiencies, but rather interoperate with other innovative technology such as artificial intelligence and cloud computing.

Remarks

Download the article as PDF-File. More information about the the Frankfurt School Blockchain Center on the Internet, on Twitter or on Facebook.

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. If you are an expert in the field and want to criticize or endorse the article or some of its parts, feel free to leave a private note here or contextually and we will respond or address.

Do you want to learn more about how blockchain will change our world?

- Blockchain knowledge: We wrote a Medium article on how to acquire the necessary blockchain knowledge within a workload of 10 working days.

About the Authors

Wanli Chen is Master of Finance graduate (Capital Markets Concentration, Class of 2019) from Frankfurt School of Finance and Management. You can contact her via mail (wanli.chen@fs-students.de) or via LinkedIn (www.linkedin.com/in/wanlichen).

Qianxia Wang is Master of Finance graduate (Corporate Finance Concentration, Class of 2019) from Frankfurt School of Finance and Management. You can contact her via mail (qianxiawang@gmail.com) or via LinkedIn (www.linkedin.com/in/qianxia-sally-wang).

References

Adams, D. (2016). Banking and Capital Markets. The College of law, Guildford, United Kingdom.

AFME (2019). AFME response to the ECB market consultation on a potential mechanism for the issuance and initial distribution of debt securities in the European Union. Retrieved from https://www.afme.eu/Reports/

Consultation-Responses.

Bloomberg (2019). Wall Street Accelerates Shake-Up in Market for New Bonds. Retrieved April 26, 2019, from https://www.bloomberg.com/news/

articles/2019-04-26/wall-street-is-said-to-accelerate-new-issue-bond-market-shake-up.

Capgemini consulting (2016). Blockchain Disruption in Security Issuance. Retrieved August 2, 2019, from https://www.capgemini.com/wp-content/

uploads/2017/07/blockchain_securities_issuance_v6_web. pdf.

Cohen, R., Smith, P., Arulchandran, V. and Sehra, A. (2018). Automation and Blockchain in Securities Issuances. Butterworths Journal of International Banking and Financial Law, 144–150.

Committee on capital markets regulation (2019). Blockchain and securities clearing and settlement. Retrieved August 04, 2019, from www.capmktsreg.org.

ECB Advisory Group on Market Infrastructures for Securities and Collateral (AMI-SECO) (2017). Cross-border market practice sub-group (XMAP) — Report on cross-CSD activity. Retrived July 10, 2019, from https://www.ecb.

europa.eu/paym/initiatives/shared/docs/d1c9d-ami-seco-2017-12-07-item-1.5-xmap-report-on-t2s-cross-csd-activity.pdf.

ECB (2018). Financial Integration in Europe. Retrieved September 11, 2019, from https://www.ecb.europa.eu/stats/financial_markets_and_interest_

rates/financial_integration/html/index.en.html.

EDDI (2019). Market Consultation on a potential Eurosystem initiative regarding a European mechanism for the issuance and initial distribution of debt securities in the European Union. European consultation launched by the European Central Bank.

ICMA (2019). ICMA responds to the ECB’s market consultation on European Distribution of Debt Instruments. Retrieved July 10, 2019, from https://www.icmagroup.org/News/news-in-brief/icma-responds-to-the-ecb-s-market-consultation-on-european-distribution-of-debt-instruments-eddi/.

ICMA (2018/2019). New fintech applications in bond markets. Retrieved August 28, 2019, from https://www.icmagroup.org/Regulatory-Policy-and-Market-Practice/fintech/new-fintech-applications-in-bond-markets/.

IFR International Financing Review (2018). Bond syndication moves into the 21st century. Retrieved July 30, 2019, from https://www.ifre.com/story/

1510191/bond-syndication-moves-into-the-21st-century-s95r30t6d1.

IHS Markit (2019). IHS Market Responds to ECB Market Consultation on EDDI. Retrieved September 07, 2019, from https://ihsmarkit.com/research-analysis/ecb-eddi-market-consultation-response.html#_ftnref2.

Lan, S.T., Ng, L., & Zhang, B.H. (2009). The World Price of Home Bias. Journal of Financial Economics, 97 (2), 191–217.

Learner, H. (2011). An examination of transparency in European bond markets. CFA Institute

Mathias Avocats (2018). Blockchain 8 main legal issues. Retrived June 30, 2019, from https://www.avocats-mathias.com/wp-content/uploads/

2018/04/LB-GM-Blockchain-Janvier-2018.pdf.

Peters, G., Panayi, E. (2015). Understanding Modern Banking Ledgers through Blockchain Technologies: Future of Transaction Processing and Smart Contracts on the Internet of Money. Retrived June 25, 2019, from https://arxiv.org/pdf/1511.05740.pdf.

Pinna, A., Ruttenberg, W. (2016). Occasional Paper Series — Distributed ledger technologies in securities post-trading, revolution or evolution? ECB Occasional Paper Series, No 172.

PreSale Ventures (2018). Can conflicting interests hold back blockchain? Retrieved July 20, 2019, from https://medium.com/@presale.venture/can-conflicting-interests-hold-back-blockchain-e63715b6ad65.

Rodriguez, J. (2019). Five challenges of permissioned blockchain solutions and the tools and protocols that can help you. Retrieved July 20, 2019, from https://hackernoon.com/five-challenges-of-permissioned-blockchain-solutions-and-the-tools-and-protocols-that-can-help-you-d3e9cf49818a.

Sandner, P., Valenta, M. (2017). Comparison of Ethereum, Hyperledger Fabric and Corda. Retrieved July 20, 2019, from https://medium.com/

@philippsandner/comparison-of-ethereum-hyperledger-fabric-and-corda-21c1bb9442f6.

Steis, M. (2019). New regulations in Europe planned for 2019 will simplify issuance of security tokens. Retrieved July 25, 2019, from https://medium.com/rockaway-blockchain/new-regulations-in-europe-planned-for-2019-will-simplify-issuance-of-security-tokens-d5e3f91c8387.